What Is the FIRE Movement in 2026?

FIRE movement 2026 is rewriting how millions of people think about work, money, and retirement — and if you’re carrying personal debt right now, this guide was written specifically for you. The FIRE movement — Financial Independence, Retire Early — is no longer just a niche internet philosophy. In 2026, it is a mainstream financial strategy pursued by salaried employees, freelancers, and entrepreneurs across India and globally, all asking the same powerful question: “What if I didn’t have to work forever?”

If you’ve ever sat at your desk on a Monday morning, sipped your third coffee, and thought “there has to be a better way” — congratulations, you’ve already had your first FIRE moment. And the good news? Even with rising personal debt on your plate, the FIRE movement 2026 roadmap has a clear, actionable path for you.

The FIRE movement — short for Financial Independence, Retire Early — is a lifestyle and financial philosophy that flips the traditional retirement script on its head. Instead of grinding until you’re 60-something and then finally “enjoying life,” FIRE followers aggressively save and invest a large portion of their income — often 40% to 70% — to reach financial independence decades earlier than the conventional retirement age.

In 2026, the FIRE movement is more relevant than ever. With inflation still nibbling at purchasing power, job insecurity creeping into every industry thanks to AI disruption, and the rising cost of living squeezing middle-class budgets globally, more people are asking: “What if I didn’t have to work forever?”

The beautiful thing about FIRE? You don’t need to be a Silicon Valley millionaire to pursue it. You just need a plan, some discipline, and — critically — a strategy for handling the elephant in the room: your debt.

The Uncomfortable Truth: Debt and FIRE Can Coexist

Here’s where most beginner guides get it wrong. They either say “pay off ALL your debt before you invest a single rupee/dollar” or they say “ignore debt and just invest.” Both extremes are oversimplified and, frankly, a little reckless.

The reality? Debt and FIRE can coexist — but they need a strategy. Not all debt is created equal. A high-interest credit card charging you 24% APR is a five-alarm financial fire (the bad kind). A low-interest home mortgage at 7% is a manageable “good debt” that doesn’t necessarily need to be obliterated before you start investing.

In 2026, the average Indian household carries personal debt across multiple categories — credit cards, personal loans, vehicle loans, education loans, and home loans. According to data trends, personal loan disbursements in India have grown significantly over the past three years, and credit card outstanding balances have hit record highs. In the US, total household debt crossed $18 trillion. The FIRE movement for beginners must, therefore, start with an honest assessment of where that debt stands — and how to manage rising personal debt while still making progress toward financial independence.

Think of it like running two engines simultaneously. One engine burns fuel to pay off your debt. The other engine builds your investment portfolio. You control the throttle on both.

Types of FIRE — Which One Is Right for You?

Before you map out your FIRE strategy, you need to know which flavor of FIRE suits your life. Here’s the 2026 breakdown:

Lean FIRE is the minimalist’s dream. You retire early but live frugally, keeping annual expenses below ₹12–15 lakhs (or $30,000–$40,000 in USD). This requires a smaller investment corpus but demands a truly lean lifestyle — think no luxuries, DIY everything, and growing your own tomatoes.

Fat FIRE is for those who want financial independence and the good life. You’re targeting a large corpus that allows annual spending of ₹30+ lakhs or $100,000+. This takes longer to achieve but gives you the most freedom.

Barista FIRE (or Semi-FIRE) is the compromise sweet spot. You reach partial financial independence and “retire” from your full-time career, but pick up part-time or passion work that covers basic expenses. Your investments grow undisturbed.

Coast FIRE is arguably the most underrated concept in 2026. You save aggressively early in your career until your invested corpus is large enough to compound on its own to your target FIRE number — without any additional contributions. You can then “coast,” working a less stressful job or reducing hours.

Slow FIRE is for the steady plodders who don’t want to dramatically cut lifestyle but make consistent, disciplined progress toward financial independence over 15–20 years.

For most people dealing with managing rising debt, Barista FIRE or Coast FIRE are the most realistic and psychologically sustainable starting points in 2026.

How Rising Personal Debt Is Derailing Early Retirement Dreams

Let’s get real for a second. Debt is the single biggest obstacle to the FIRE movement for beginners in 2026 — and it’s getting worse.

In India, “Buy Now, Pay Later” (BNPL) schemes have exploded, personal loan apps have made borrowing dangerously easy, and lifestyle inflation has pushed millions into the “paycheck to paycheck” trap despite decent salaries. In Western markets, student loan debt remains a generational burden, auto loan terms have stretched to 84 months (seven years!), and credit card interest rates have climbed to record highs.

When you’re paying interest on multiple debts simultaneously, you’re essentially running a race with weights tied to your ankles. Every rupee that goes to interest is a rupee that could have been compounding in your investment portfolio.

Here’s a sobering example: If you carry ₹5 lakhs of credit card debt at 36% annual interest and only make minimum payments, you’ll pay more in interest over five years than the original debt itself. Meanwhile, that same ₹5 lakhs invested in an index fund at a 12% annual return over 20 years becomes approximately ₹48 lakhs. The cost of not addressing debt is not just the interest — it’s the opportunity cost of every rupee trapped in repayment.

This is precisely why the FIRE movement 2026 demands a dual-track strategy. You cannot afford to ignore debt, and you cannot afford to ignore investing. You must do both.

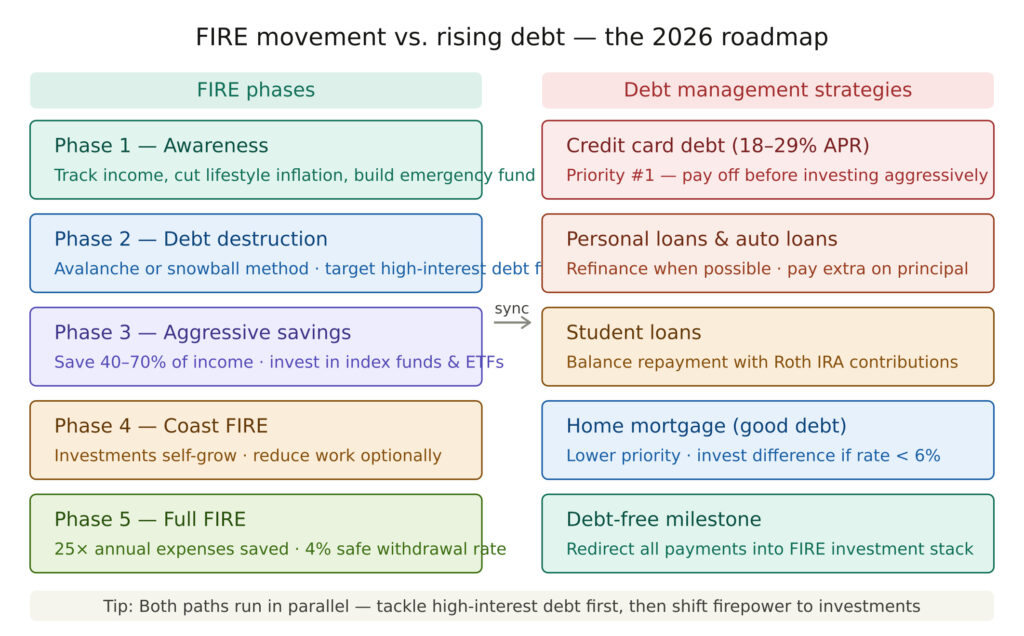

The FIRE + Debt Freedom Blueprint — Running Both Tracks Simultaneously

Here is the practical blueprint that thousands of successful FIRE followers use to manage both debt payoff and wealth building at the same time:

Track 1: The Debt Paydown Engine

Start by listing every single debt you carry — the balance, the interest rate, and the minimum monthly payment. Now apply one of two proven methods:

The Debt Avalanche Method targets the highest interest-rate debt first while making minimum payments on everything else. Mathematically, this is the fastest way to reduce total interest paid and it’s the approach most strongly recommended for FIRE followers. That 24–36% credit card APR is a monster — kill it first.

The Debt Snowball Method targets the smallest balance first regardless of interest rate. The psychological wins from eliminating debts one by one can keep motivation high. Choose this if you’ve previously struggled with staying the course.

Track 2: The Investment Engine

Even while aggressively paying down debt, do not completely stop investing. Here’s why: in 2026, if your employer offers any form of retirement contribution match — whether that’s a PF contribution match or a 401(k) match — that is effectively a 50–100% instant return on your money. Always capture the full match, period.

Beyond that, contribute to your Roth IRA (or NPS in India) and index fund portfolio with whatever you can consistently set aside — even if it’s just 5–10% of income while you’re in heavy debt-payoff mode. The habit of investing is as important as the amount.

The thumb rule for 2026: If your debt carries an interest rate above 8–10%, prioritize paying it down. If below that threshold, consider investing the difference since long-term equity returns historically outperform that rate.

Step-by-Step: Paying Off Debt While Building Your FIRE Number

Here’s a concrete step-by-step action plan for someone starting their FIRE movement journey in 2026 while carrying personal debt:

Step 1: Calculate your FIRE number. Multiply your annual expenses by 25. This is the corpus you need to retire early using the 4% rule. If you spend ₹8 lakhs per year, your FIRE number is ₹2 crores. Write this down. Pin it somewhere visible.

Step 2: Build a 3-month emergency fund first. Before aggressively attacking debt or investing, ensure you have 3 months of expenses in a liquid savings account or liquid mutual fund. This prevents you from going back into debt when an emergency strikes.

Step 3: Attack high-interest debt relentlessly. Using the debt avalanche method, throw every extra rupee at your highest-rate debt. Cut subscriptions, reduce dining out, pause non-essential spending temporarily. This phase is painful — but it is also temporary.

Step 4: Simultaneously capture “free money.” Always contribute enough to your EPF/PPF or employer-matched retirement account to capture the full employer match. This is non-negotiable even during debt-payoff mode.

Step 5: Once high-interest debt is cleared, shift gears. Now redirect former debt payments into your investment portfolio. Automate SIPs into diversified equity mutual funds or index funds. The amount that was going to your loan EMI should now go straight to wealth building.

Step 6: Track your FIRE progress quarterly. Use a net worth tracker, a FIRE calculator app, or a simple spreadsheet. Watching your net worth grow is incredibly motivating and keeps you on track.

FIRE Movement 2026 by the Numbers — What the Data Actually Says

One of the most common questions people ask when they first discover the FIRE movement 2026 is: “Is this actually working for real people, or is it just a motivational fantasy sold by finance influencers?”

Fair question. So let’s talk data — because the numbers tell a genuinely compelling story.

According to surveys conducted across FIRE communities globally, the median age at which people successfully achieve financial independence and retire early sits between 37 and 45 years — a full two decades ahead of the conventional retirement age of 60–65. That’s 20 extra years of waking up on your own terms. Two decades of not checking your leave balance before booking a holiday.

Here is what the FIRE movement 2026 landscape looks like when you zoom out and look at the macro picture:

Savings rate vs. years to retirement is the most eye-opening data point for beginners. The relationship is not linear — it’s dramatically accelerating:

| Savings Rate | Approximate Years to FIRE |

|---|---|

| 10% | 43 years |

| 20% | 37 years |

| 30% | 28 years |

| 40% | 22 years |

| 50% | 17 years |

| 60% | 12.5 years |

| 70% | 8.5 years |

The math is unambiguous. Every 10% increase in your savings rate shaves years — sometimes an entire decade — off your working life. This is why the FIRE movement 2026 places such intense emphasis on savings rate over income level. A person earning ₹15 lakhs and saving 50% will reach financial independence faster than a person earning ₹40 lakhs and saving 10%.

Now layer in the debt dimension. Research consistently shows that households carrying high-interest consumer debt — credit cards, personal loans above 15% APR — take an average of 4 to 7 additional years to reach their FIRE number compared to debt-free households with the same income. That is not a small penalty. That is nearly a decade of your life lost to interest payments.

This is the clearest argument for why the FIRE movement 2026 must begin with an aggressive debt destruction phase, particularly targeting any debt above the 10% interest threshold. Every month you delay paying off a 24% credit card is not just a financial loss — it is time leaving your life.

The silver lining? Among people who actively combined debt payoff with consistent investing — the dual-track approach — the average time penalty was reduced to just 1.5 to 2 years compared to debt-free FIRE pursuers. Running both tracks simultaneously is not just possible. The data says it is nearly as effective as starting debt-free.

One more number worth tattooing on your brain: the power of the first ₹10 lakhs (or first $50,000 for US readers). Financial independence research and community data consistently show that the journey from zero to your first major portfolio milestone is the hardest, slowest stretch. After that, compounding takes over and the portfolio begins to grow faster than your contributions. Getting through the early debt-heavy phase to reach that first milestone is the hardest part of the FIRE movement 2026 journey — and also the most important.

Push through. The compounding engine on the other side is waiting.

The 4% Rule — Still Valid in 2026?

The 4% rule is the backbone of almost every FIRE strategy. It states that if you withdraw 4% of your investment portfolio in the first year of retirement and adjust annually for inflation, your portfolio has a high probability of lasting 30+ years.

The rule originated from the famous 1994 Trinity Study, which analyzed historical US market data. In 2026, there’s been ongoing debate about whether 4% is still safe given higher valuations, lower expected returns, and sequence-of-returns risk in a volatile global economy.

The emerging consensus among financial planners in 2026 is to use a slightly more conservative 3.5% withdrawal rate if you plan to retire very young (say, before 40) and have a 40–50 year retirement horizon. For those targeting retirement in their late 40s to early 50s, the 4% rule remains a reasonable planning benchmark.

For Indian FIRE followers, the equation is more nuanced. India’s inflation rate has historically been higher, but equity returns (Sensex/Nifty long-term averages) have also been higher. A 3–3.5% withdrawal rate from a well-diversified portfolio including Indian equities, international equity exposure, and some debt instruments is considered prudent for early retirement in India in 2026.

FIRE Movement for Beginners: Your First 90 Days

If you’re brand new to the FIRE movement in 2026 and feeling overwhelmed, here’s your first 90-day action plan — no finance degree required:

Days 1–30: Awareness and audit. Track every rupee you spend for 30 days. Use an app like Walnut, Money Manager, or even a Google Sheet. Calculate your savings rate (savings divided by take-home income). The average FIRE follower targets a minimum 30% savings rate — where are you now?

Days 31–60: The debt and income inventory. List all debts with balances and interest rates. List all income sources. Calculate your current net worth (assets minus liabilities). If it’s negative, that’s okay — knowing your starting point is powerful.

Days 61–90: Build your personal FIRE plan. Choose your FIRE variant (Lean, Barista, Fat, Coast). Calculate your FIRE number. Set up automated debt payments and automated SIP investments, even if small. Open a Zerodha, Groww, or Vanguard account if you haven’t already. Start.

The biggest mistake beginners make is waiting until conditions are “perfect” before starting. They’re not going to be perfect. Start messy. Start now.

Real-World FIRE Case Study — From ₹45L Debt to Early Retirement in 7 Years

Consider Arun and Priya, a couple in their early 30s from Pune. In 2019, they had a combined income of ₹28 lakhs per year but carried ₹45 lakhs in total debt — a home loan, two car loans, personal loans, and credit card dues. Retirement felt like a fantasy.

They discovered the FIRE movement and committed to a dual-track approach. They sold one of the cars, stopped dining out, cancelled unused subscriptions, and switched to term insurance from expensive traditional plans. They threw an extra ₹40,000 per month at their highest-interest debt (a personal loan at 18%) while simultaneously investing ₹15,000/month in Nifty 50 index funds via SIP.

By 2022, the personal loan and credit cards were gone. They redirected that ₹40,000/month entirely into equity mutual funds. By 2026, their combined investment portfolio has crossed ₹1.2 crores, their home loan balance has dropped to ₹12 lakhs, and they’re on track for Barista FIRE by age 40.

Their combined annual savings rate? 58%.

The lesson: managing rising personal debt is not the end of your FIRE dream — it can be the beginning of your most disciplined financial chapter.

Common FIRE Movement 2026 Myths That Are Quietly Killing Your Progress

If you have spent any time reading about the FIRE movement 2026 online, you have almost certainly encountered some deeply misleading advice wrapped in motivational packaging. Some of these myths are harmless. Others are genuinely dangerous to your financial future. Let’s dismantle the most damaging ones right now — because half of the people who fail to achieve financial independence retire early do so not from lack of effort, but from following the wrong map.

Myth 1: “You need a six-figure income to pursue FIRE.”

This is the most widespread and most damaging myth in the FIRE movement 2026 space. The truth? Your savings rate matters infinitely more than your income. Mr. Money Mustache — arguably the most famous FIRE success story globally — retired at 30 on a combined household income that was solidly middle-class. In the Indian context, numerous documented cases exist of individuals on ₹8–12 lakh annual salaries achieving Lean FIRE by their early 40s through disciplined saving and index fund investing. Income accelerates the journey. It does not determine whether the journey is possible.

Myth 2: “Pay off ALL debt completely before you invest a single rupee.”

We touched on this earlier, but it deserves its own spotlight here because it is repeated so confidently in so many beginner finance spaces. This advice ignores the mathematics of opportunity cost entirely. If you spend five years paying off a home loan at 8.5% interest before investing a single rupee, you have lost five years of compounding on an equity portfolio that historically returns 11–13% in India over the long term. The FIRE movement 2026 framework says: eliminate high-interest toxic debt immediately, manage low-interest debt in parallel with investing, and never stop investing entirely.

Myth 3: “FIRE means you never work again.”

This one is more philosophical than financial, but it matters. Many FIRE achievers continue to work — just on projects they choose, at a pace they set, for causes they care about. The “retire early” in Financial Independence Retire Early is better understood as “retire from mandatory work.” You may write a book, consult part-time, start a small business, or volunteer. The critical difference is that financial pressure no longer drives those decisions. In 2026, with remote work and the gig economy creating more flexible income options than ever, the lines between “retired” and “working on your own terms” have blurred beautifully.

Myth 4: “The stock market is too risky for FIRE — I’ll stick to FDs and gold.”

In an era of 5–6% fixed deposit returns against a 5–6% inflation rate, keeping your long-term wealth entirely in FDs means your real return is approximately zero. Gold has its place as a small portfolio hedge — but it generates no income and has historically underperformed equity over 20-year periods. The FIRE movement 2026 requires long-term equity exposure — diversified index funds, Nifty 50, S&P 500 equivalents — to generate the real returns needed for financial independence. Avoiding equity entirely is not safety. It is a slower, quieter form of financial self-sabotage.

Myth 5: “I missed the right age to start — FIRE isn’t for me anymore.”

Starting at 40 is better than starting at 45. Starting at 45 is better than starting at 50. The compounding math always favors starting sooner, but it never closes the door entirely on those who start later. A 42-year-old who aggressively implements the FIRE movement 2026 framework can realistically target Barista FIRE or Lean FIRE by 55 — still a decade ahead of conventional retirement, with dramatically more financial security than if they had never started at all. The enemy of FIRE is not age. It is inaction.

Busting these myths is not just an intellectual exercise. Every one of these misconceptions represents a roadblock that has kept real people from starting their FIRE movement 2026 journey. Remove the roadblock. Start the journey.

Tools, Apps & Resources to Supercharge Your FIRE Journey

A few trusted tools to help you in 2026:

For tracking spending and net worth, YNAB (You Need A Budget), Walnut (India), or a custom Google Sheets template work brilliantly.

For investing in India, Zerodha Coin for direct mutual funds, Groww for index funds, and the NPS portal for tax-efficient retirement contributions are strong choices.

For US-based FIRE followers, Vanguard, Fidelity, or Charles Schwab for low-cost index fund investing. The Personal Capital (Empower) dashboard is excellent for net worth tracking.

For FIRE calculators, the FIRECalc tool, cFIREsim, and the RRI calculator on Freefincal are highly regarded for stress-testing your retirement plan against historical market scenarios.

For community and motivation, the r/financialindependence subreddit, the Indian FIRE community on Asan Ideas for Wealth, and various FIRE-focused YouTube channels offer real stories, debates, and tactical advice.

Frequently Asked Questions (FAQs)

Q: Can I pursue the FIRE movement 2026 goals while still paying off debt?

Absolutely — and this is actually one of the most searched questions among beginners exploring the FIRE movement 2026 for the first time. The key is prioritizing high-interest debt (anything above 10% APR) while simultaneously capturing your employer’s retirement contribution match and building a consistent — even if small — investment habit. The FIRE movement 2026 framework is specifically designed for dual-track execution. Debt payoff and wealth building are not mutually exclusive. They are two engines running in parallel, and the sooner you start both, the sooner you cross the finish line.

Q: What savings rate do I need to make the FIRE movement 2026 work for me?

Most serious FIRE movement 2026 followers target a savings rate between 40% and 70% of take-home income. That said, even a committed 30% savings rate is a powerful and meaningful start — especially when you are simultaneously managing debt obligations. The higher your savings rate, the faster your FIRE movement 2026 journey accelerates: a 50% savings rate gets you to financial independence in roughly 17 years from zero net worth, while a 70% rate can compress that timeline to under 9 years. Start wherever you are, then push the rate up by 1–2% every six months as debts get cleared.

Q: Is the FIRE movement 2026 realistic for salaried employees in India?

Yes — and 2026 may actually be the best year yet for Indian salaried professionals to begin their FIRE movement 2026 journey. The explosion of low-cost index funds, zero-commission SIP platforms like Groww and Zerodha Coin, and growing financial literacy communities makes it more accessible than ever before. That said, the FIRE movement 2026 is not exclusive to Tier-1 city tech salaries. Even moderate-income earners in Tier-2 cities can meaningfully pursue Lean FIRE or Barista FIRE with disciplined saving, lower cost of living, and consistent equity investing. The FIRE number simply scales with your lifestyle — which is entirely within your control.

Q: Should I invest in real estate or stocks as part of my FIRE movement 2026 strategy?

This is one of the most debated questions in the FIRE movement 2026 community — and the honest answer is: it depends on the numbers, not emotions. A diversified approach generally works best. Equity mutual funds and index funds (Nifty 50, S&P 500 equivalents) form the core growth engine of most successful FIRE movement 2026 portfolios because of their liquidity, low cost, and historical long-term returns. Real estate can complement this — but only if the property generates genuine positive cash flow after EMI, maintenance, and vacancy costs. Buying real estate purely for appreciation speculation is a trap that has delayed many FIRE movement 2026 journeys by years, locking up capital in illiquid assets that generate no income.

Q: What is the single biggest mistake people make in their FIRE movement 2026 journey?

After studying thousands of FIRE movement 2026 case studies and community experiences, two mistakes surface repeatedly. First, dramatically underestimating healthcare and medical costs in early retirement — especially for those retiring before employer-sponsored health coverage kicks in. Healthcare inflation consistently outpaces general inflation, and a single major medical event without adequate cover can devastate a carefully built FIRE corpus. Second, withdrawing too aggressively in the early years of retirement during a market downturn — known as sequence-of-returns risk — which can permanently impair a portfolio’s ability to recover. Every serious FIRE movement 2026 plan should include a 1–2 year liquid expense buffer fund held outside equity markets, plus a comprehensive health insurance policy secured well before retirement.

External Resources for Financial Learning

For official information about financial planning and investor awareness, you can explore:

Do Follow External Links:

These organizations provide reliable financial education resources.

Related Articles

- Common Investment Mistakes Beginners Should Avoid in 2026

- Emergency Fund in India: Ultimate Step-by-Step Guide to Build Financial Safety in 2026

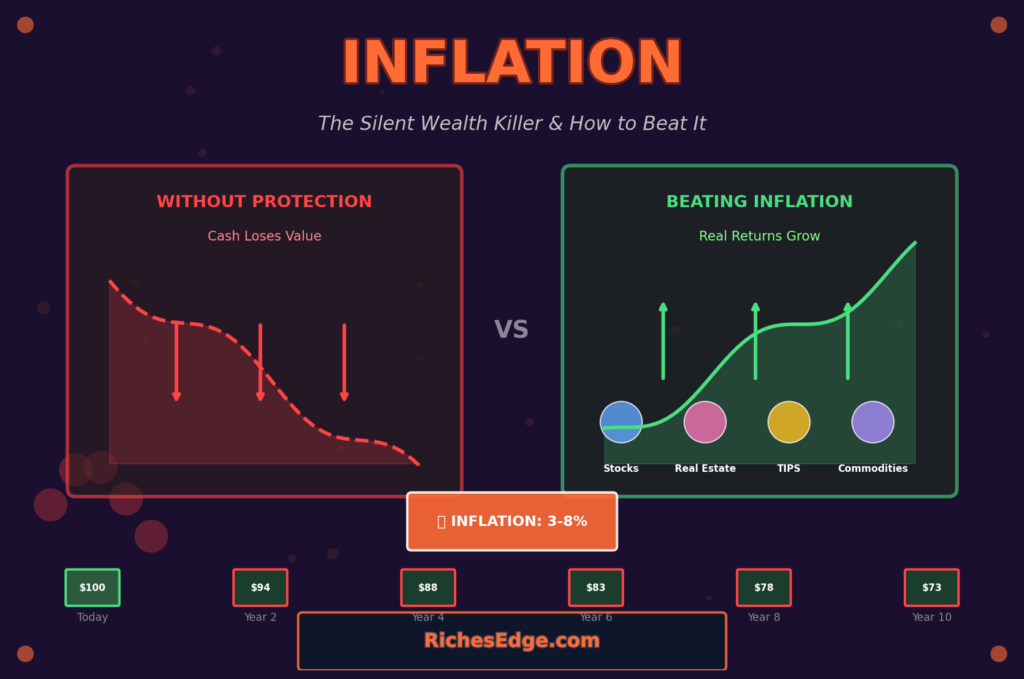

- How Inflation Affects Your Investments (And How to Beat It)

Final Word: Light Your FIRE, Don’t Let Debt Blow It Out

Look, the FIRE movement in 2026 isn’t about deprivation, extreme frugality, or giving up every joy in life. It’s about intentionality — deciding what your money does for you, rather than letting debt, lifestyle inflation, and inertia make that decision by default.

Managing rising personal debt while pursuing early retirement is genuinely hard. It requires sacrifice, patience, and a healthy dose of delayed gratification. But the payoff? Waking up every morning and choosing how you spend your time — not because your EMI demands it, but because you’ve built the financial freedom to decide.

Whether you’re drowning in credit card bills, halfway through a home loan, or just starting to think about what “financially independent” even means — the FIRE movement has a version that works for you.

Start where you are. Use what you have. Do it now.

The flame doesn’t light itself. But once it does? It’s worth every hard month it took to get there. 🔥