Introduction to Direct vs Regular Mutual Funds

Direct vs Regular Mutual Funds is one of the most searched questions among new investors in India. When you begin your investment journey in mutual funds, you will notice that almost every fund has two plan options — Direct Plan and Regular Plan.

At first glance, they may appear identical because both invest in the same portfolio and follow the same fund manager strategy. However, there is one major difference that can significantly impact your long-term wealth: cost and commission.

Understanding the difference between direct and regular mutual funds can help you:

- Increase long-term returns

- Reduce investment costs

- Choose the right investment approach

In this detailed beginner-friendly guide, we will explore Direct vs Regular Mutual Funds, their differences, advantages, disadvantages, and which option is best for you in 2026.

What Are Mutual Fund Plans?

Before understanding the difference between direct vs regular mutual funds, it is important to understand how mutual funds work.

A mutual fund collects money from many investors and invests it in assets like:

- Stocks

- Bonds

- Government securities

- Money market instruments

These funds are managed by professional fund managers who aim to generate returns based on the fund’s objective.

In India, mutual funds are regulated by Securities and Exchange Board of India and promoted by Association of Mutual Funds in India, ensuring investor protection and transparency.

However, each mutual fund scheme offers two investment routes:

- Direct Plan

- Regular Plan

Let’s understand them individually.

What Is a Direct Mutual Fund?

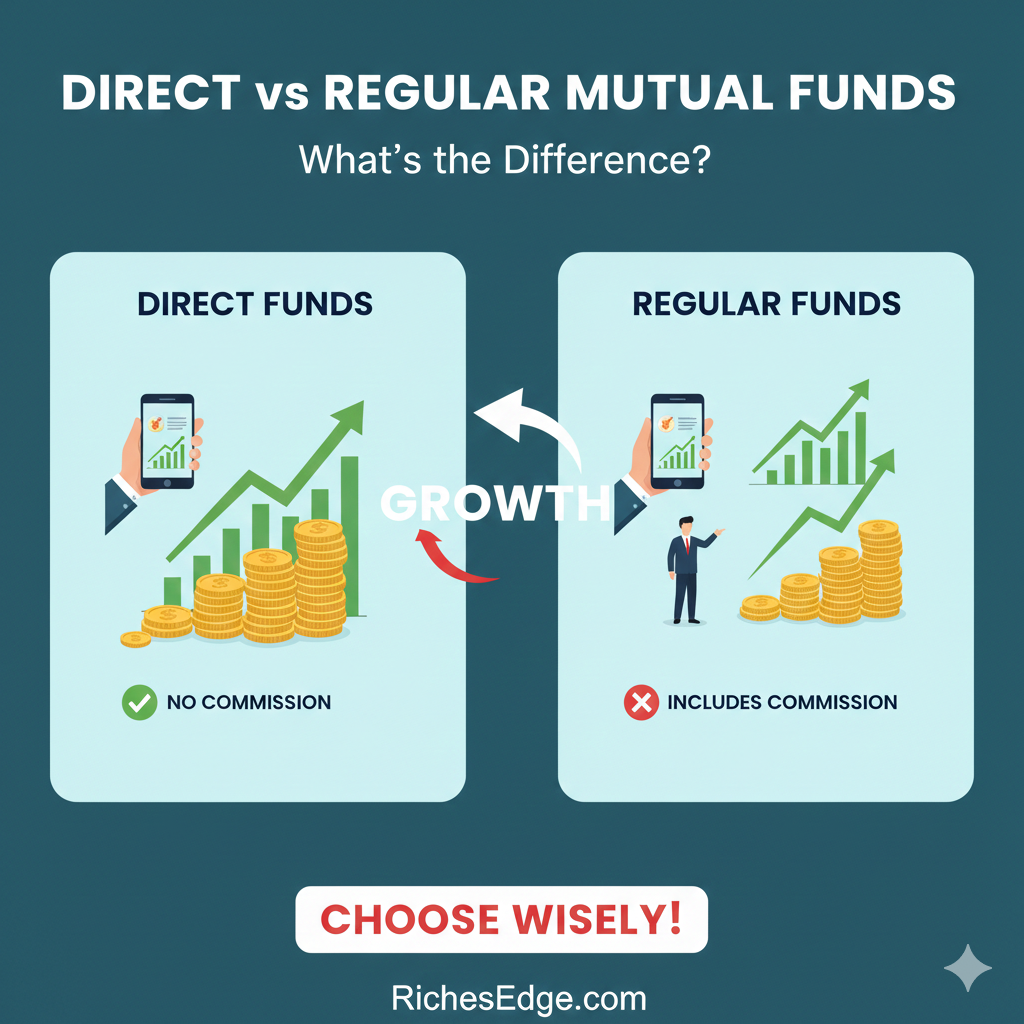

A Direct Mutual Fund Plan allows investors to invest directly with the mutual fund company without involving any distributor, broker, or agent.

This means:

- No commission is paid to intermediaries

- Expense ratio is lower

- Returns are slightly higher over time

Investors can purchase direct mutual funds through:

- AMC official websites

- Investment apps

- Online mutual fund platforms

Because commissions are removed, direct mutual funds typically generate 0.5% to 1% higher returns annually compared to regular plans.

What Is a Regular Mutual Fund?

A Regular Mutual Fund Plan is purchased through an intermediary such as:

- Mutual fund distributors

- Financial advisors

- Banks

- Investment brokers

In this model, the mutual fund company pays a commission to the distributor for bringing investors to the fund.

This commission is included in the expense ratio, which reduces the investor’s net returns.

However, regular plans provide professional guidance, making them useful for beginners who need financial advice.

Direct vs Regular Mutual Funds: Key Differences

Below is a simplified comparison to understand the difference between direct and regular mutual funds.

| Feature | Direct Mutual Funds | Regular Mutual Funds |

|---|---|---|

| Purchase Method | Direct from AMC | Through distributor |

| Commission | No commission | Distributor commission included |

| Expense Ratio | Lower | Higher |

| Returns | Slightly higher | Slightly lower |

| Advisory Support | No advisor | Advisor support available |

| Suitable For | Experienced investors | Beginners |

Although both plans invest in the same portfolio, the expense ratio difference makes a big impact over time.

Expense Ratio and Its Impact on Returns

The expense ratio represents the annual fee charged by the mutual fund to manage investments.

It includes costs like:

- Fund management fees

- Administrative expenses

- Distribution commissions

In regular mutual funds, distributor commissions increase the expense ratio.

Example:

Direct Plan Expense Ratio: 1.0%

Regular Plan Expense Ratio: 1.8%

That 0.8% difference may seem small, but over long-term investing it can significantly reduce your returns.

Example: Direct vs Regular Mutual Fund Returns

Let’s assume an investor invests ₹10,000 per month for 20 years.

Expected return: 12% annually

Approximate outcome:

Direct Plan Investment Value: ₹1.0+ crore

Regular Plan Investment Value: ₹90–94 lakhs

The difference of ₹6–10 lakhs occurs mainly because of the commission embedded in regular mutual funds.

This example clearly shows why many experienced investors prefer direct mutual funds.

Pros and Cons of Direct Mutual Funds

Advantages

Higher returns due to lower expense ratio

No distributor commission

Full transparency in investment

Suitable for DIY investors

Disadvantages

No professional financial advice

Requires personal research

Risk of choosing wrong funds without guidance

Direct plans are best suited for investors who:

- Understand mutual funds

- Can research funds independently

- Prefer lower costs

Pros and Cons of Regular Mutual Funds

Advantages

Higher returns due to lower expense ratio

No distributor commission

Full transparency in investment

Suitable for DIY investors

Disadvantages

No professional financial advice

Requires personal research

Risk of choosing wrong funds without guidance

Direct plans are best suited for investors who:

- Understand mutual funds

- Can research funds independently

- Prefer lower costs

Which Is Better: Direct or Regular Mutual Funds?

There is no universal answer to which is better: direct or regular mutual funds.

It depends on the investor’s experience and comfort level.

Choose Direct Mutual Funds if:

- You understand investing

- You research funds independently

- You want maximum long-term returns

Choose Regular Mutual Funds if:

- You are a beginner

- You want professional financial advice

- You prefer guided investing

Many investors initially start with regular plans and later shift to direct plans once they gain confidence.

How to Invest in Direct Mutual Funds

Investing in direct mutual funds has become very easy in India.

You can invest through:

Mutual fund company websites

Online investment platforms

Mobile investment apps

Basic steps include:

- Complete KYC verification

- Choose mutual fund scheme

- Select Direct Plan

- Invest via SIP or lump sum

Always verify that the plan selected is Direct, otherwise it will default to Regular Plan.

Common Mistakes Investors Make

While choosing between direct vs regular mutual funds, investors often make mistakes.

1 Choosing funds only based on returns

Past returns do not guarantee future performance.

2 Ignoring expense ratio

Even small fee differences affect long-term wealth.

3 Investing without diversification

Avoid putting all money in one scheme.

4 Not reviewing investments

Review mutual fund portfolios at least once per year.

Expert Tips for Beginners

If you are new to mutual fund investing, follow these tips:

Start with SIP investing

Choose diversified equity funds

Invest for long-term goals

Avoid reacting to short-term market volatility

Review funds annually

Most importantly, focus on consistent investing rather than timing the market.

Related Articles

- Best Mutual Funds for Beginners in India

- Debt vs Equity Mutual Funds: Which One Should You Choose?

- Index Funds vs Active Funds: Which Is Better for Long-Term Investors?

Final Thoughts

Understanding Direct vs Regular Mutual Funds is essential for every investor starting their financial journey.

While both plans invest in the same portfolio, the cost structure makes a meaningful difference in long-term returns.

Direct plans provide higher returns due to lower expense ratios, while regular plans offer professional guidance and convenience.

For beginners, regular plans can provide helpful guidance. However, as investors gain knowledge and confidence, switching to direct mutual funds can help maximize wealth creation over time.

Ultimately, the best choice depends on your investing knowledge, comfort level, and financial goals.